You have 0 items in your cart

Planning for Incapacity and Beyond: Why You Need Both

When clients first come to my office, they often ask: “Do I need a power of attorney or a trust?” The truth is, this isn’t an either/or question. Understanding how a power of attorney revocable trust strategy works together is essential for complete protection.

Let me break it down simply:

| Document | Primary Purpose | When Active | Ends At | Controls |

|---|---|---|---|---|

| Power of Attorney | Gives someone authority to act on your behalf | During life (while capable or incapacitated) | Your death | Assets in your name only |

| Revocable Trust | Creates legal entity to hold and manage assets | During life and after death | When trust terms complete | Only assets titled to the trust |

Think of your estate plan like protecting your home. Your power of attorney is like giving a trusted friend a spare key to your front door, while your revocable trust is like building a secure room inside where your most valuable items are stored. Both serve important but different functions.

I’ve seen too many families find gaps in their planning at the worst possible moment. Without both documents working together, you’re leaving yourself vulnerable.

Why a combined power of attorney revocable trust approach matters:

Your power of attorney becomes completely ineffective the moment you pass away, leaving no authority for handling affairs afterward. Meanwhile, your beautifully crafted revocable trust only controls what you’ve actually transferred into it—often leaving significant assets unprotected.

I’ve witnessed frustrated family members find that Dad’s power of attorney (created 15 years ago) is being rejected by his bank, or that Mom’s trust was perfectly drafted but never funded with her assets. These situations often lead to expensive court proceedings that could have been avoided.

My name is Michael Hurckes, and after guiding hundreds of clients through establishing comprehensive incapacity planning, I’ve learned that proper coordination between these documents prevents not just legal complications, but family stress during already difficult times.

Having a comprehensive plan that includes both a power of attorney revocable trust strategy provides the peace of mind that comes from knowing you’ve covered all bases. Whether you need a simple will and power of attorney or more complex planning involving Medicaid estate planning, the key is ensuring these documents work together seamlessly.

Many clients worry about the complexity or cost of creating multiple documents, but lawyers specializing in trusts and wills can help make this process straightforward and affordable. The cost of planning now is minimal compared to the potential expense and heartache of court proceedings later.

Understanding the Basics: Power of Attorney vs. Revocable Living Trust

Let’s take a moment to understand these two powerful legal tools before we explore how they work together. Think of it this way: a power of attorney creates a relationship where someone can act for you, while a revocable living trust creates an actual legal entity that can own your stuff.

What Is a Power of Attorney?

A power of attorney (POA) is essentially permission for someone you trust (your “agent”) to handle your affairs. When you create a POA, you’re the “principal” – the person giving authority to someone else.

Picture your POA as a legal permission slip that says, “This person can sign my name and make decisions for me.” The scope of this permission slip varies based on the type you choose:

A general power of attorney gives broad authority but stops working if you become incapacitated – not ideal for long-term planning. A durable power of attorney contains special language ensuring it continues working even if you can’t make decisions anymore – making it the most useful for most people.

Some folks prefer a springing power of attorney, which only “springs” into effect when a specific event happens, usually when a doctor confirms you can’t make decisions. While this sounds appealing, it can create practical problems when your agent needs to prove your incapacity to skeptical banks or institutions.

Here’s the crucial part that many people miss: all powers of attorney become worthless when you die. They’re powerful tools during your lifetime but completely ineffective afterward.

Without a proper POA in place, your family might need to go through an expensive and public court process to get authority over your affairs if you become incapacitated. This court-supervised arrangement (called guardianship or conservatorship) can be avoided with a well-drafted POA.

For more details about how powers of attorney work alongside wills, check out our page on simple will and power of attorney.

What Is a Revocable Living Trust?

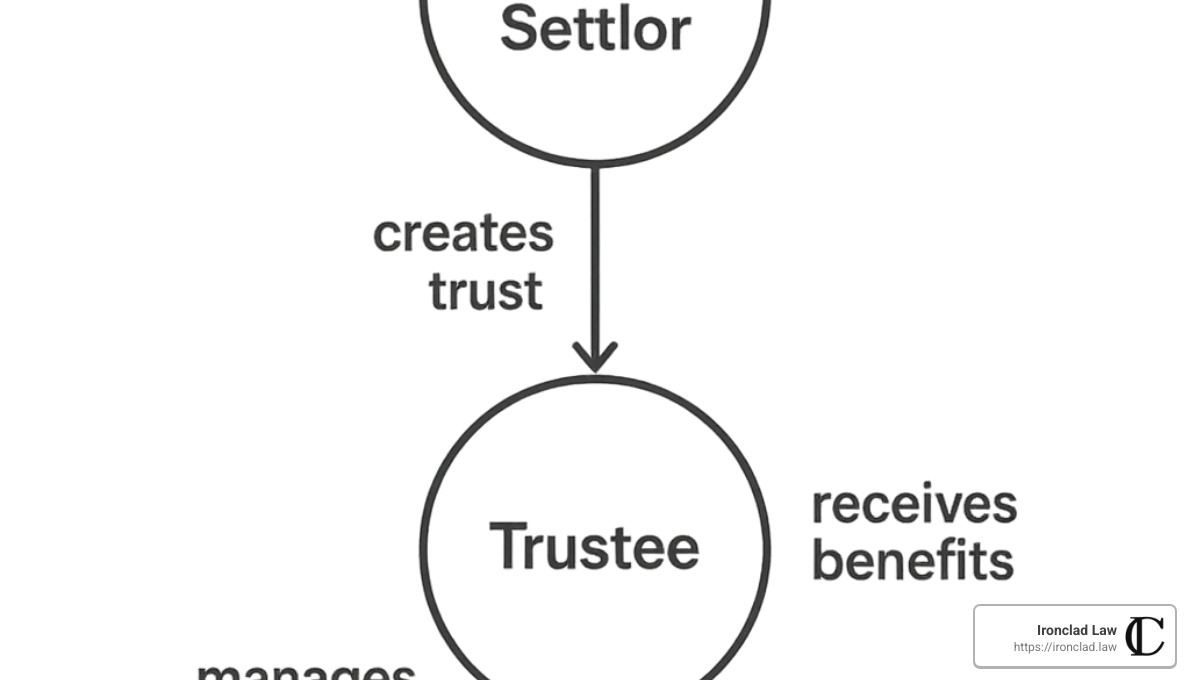

A revocable living trust creates a separate legal container for your assets. When you establish this trust, you typically wear three hats:

- You’re the grantor (or settlor) who creates and funds the trust

- You’re the trustee who manages the assets inside the trust

- You’re the beneficiary who enjoys the benefits of those assets

The beauty of this arrangement is that you maintain complete control while creating a seamless transition plan for both incapacity and death. You can change or cancel the trust anytime during your lifetime, which is why it’s called “revocable.”

One major advantage of a power of attorney revocable trust strategy is privacy protection. Unlike wills that become public record through probate, your trust terms remain private. Plus, properly funded trusts avoid probate entirely, saving your loved ones time, money, and stress.

However, creating the trust is only half the battle. You must actually transfer ownership of your assets into the trust – a process called “funding” – for it to work properly. This typically means changing titles on bank accounts, real estate, and other assets to show the trust as the owner.

Most people also create a “pour-over will” alongside their trust. This special will acts as a safety net, directing any forgotten assets into your trust after death. While these assets would still go through probate, at least they’d ultimately follow your trust instructions.

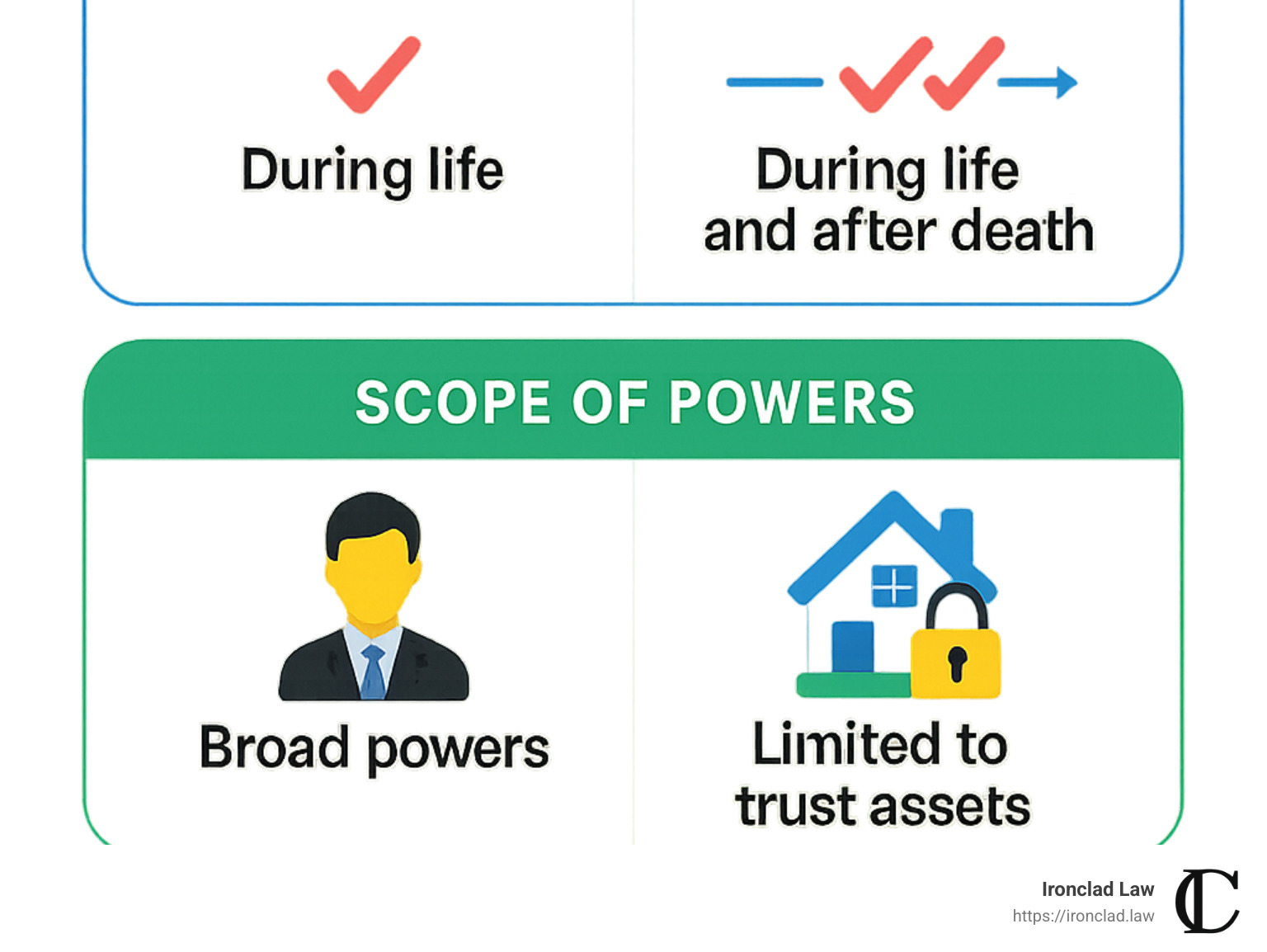

Remember this key difference: a power of attorney helps manage assets in your name during life, while a trust manages assets in its name both during life and after death.

Power of Attorney Revocable Trust: Key Differences

When setting up your estate plan, understanding the differences between a power of attorney revocable trust arrangement can save your family significant stress and expense. These two legal tools serve different purposes and work in complementary ways.

Here’s how they compare on the essentials:

| Feature | Power of Attorney | Revocable Trust |

|---|---|---|

| Legal Ownership | Principal retains ownership | Trust owns the assets |

| Who Controls | Agent acts on principal’s behalf | Trustee manages trust property |

| Court Oversight | No regular supervision | No regular supervision |

| Effective Period | During life only | During life and after death |

| Incapacity Planning | Requires “durable” language | Built-in with successor trustee |

| Privacy | Generally private | Completely private |

| Probate Avoidance | No | Yes (for funded assets) |

| Institutional Acceptance | Often challenged | Rarely questioned |

Scope of Authority Under a Power of Attorney Revocable Trust

The way authority works differs dramatically between these two legal tools, which is why many people benefit from having both.

With a power of attorney, your agent steps into your shoes legally speaking. They sign documents as “[Your Name], by [Agent Name], Attorney-in-Fact” – essentially acting as you. However, their powers are strictly limited to what’s explicitly written in your document.

Many states require specific “hot powers” to be expressly authorized in the document. These include important abilities like making gifts, creating or changing trusts, updating beneficiary designations, or disclaiming inheritances. Without these explicitly stated, your agent’s hands may be tied when they need flexibility the most.

A significant practical problem is that banks and financial institutions often reject powers of attorney, especially older ones. As the American Bar Association notes, “Financial institutions often reject older powers of attorney, which can create significant barriers to managing assets for incapacitated individuals.” This can happen even when your document is legally valid, leaving your family in a difficult position.

With a revocable trust, the dynamics are different. Your trustee signs as “Trustee of the [Your Name] Revocable Trust dated [date]” and has clear authority over trust-owned assets. The trustee must follow the trust’s terms and has a legal duty (called a fiduciary duty) to manage assets appropriately.

Financial institutions rarely question a properly documented trustee’s authority, making a trust a more reliable tool when immediate action is needed. This reliability is one reason many estate planning attorneys recommend trusts for clients concerned about potential incapacity.

Duration & Continuity in a Power of Attorney Revocable Trust

Perhaps the most important difference between these tools is how long they last:

A power of attorney stops working the moment you die – no exceptions. This creates a potential gap in management authority that can cause problems for your family. Additionally, even during your lifetime, financial institutions might reject your power of attorney if they consider it “stale” or too old. If you want to change agents, you’ll need to create an entirely new document.

A revocable trust, on the other hand, continues seamlessly after your death. The trust remains effective until all assets are distributed according to your instructions. You can include detailed plans for multiple generations and create a smooth transition between successor trustees without court involvement.

This continuity is why many estate planning attorneys recommend a revocable trust as the foundation of a comprehensive estate plan, particularly if you have substantial assets or a complex family situation. The trust provides an uninterrupted management structure that works during incapacity and continues after death – something a power of attorney simply cannot do.

That said, a well-crafted power of attorney revocable trust strategy uses both tools together to cover all bases. Your power of attorney handles assets not yet transferred to your trust, while your trust provides long-term management for your most important property.

Coordinating Your Documents for Incapacity Planning

When it comes to protecting yourself during incapacity, having both a power of attorney revocable trust arrangement gives you the most comprehensive coverage. But these documents need to work together seamlessly – like dance partners who know each other’s moves.

Can a Power of Attorney Manage Trust Assets?

Here’s a surprise that catches many people off guard: A power of attorney generally cannot be used to manage assets held in a revocable living trust.

Why not? It’s all about legal ownership. Trust assets aren’t technically owned by you anymore – they’re owned by the trustee (even if that’s also you). Your agent under a power of attorney only has authority over assets in your individual name.

As one of our clients recently finded when trying to help her mother: “I had the power of attorney in hand, but the bank wouldn’t let me touch the trust accounts. It was frustrating because we thought we had everything covered.”

To avoid this situation, consider these approaches:

Name your agent as successor trustee so they have direct authority over trust assets if you become incapacitated. This creates a clear line of authority without any confusion.

Keep some assets outside the trust with POD (payable on death) designations. This gives your agent something to work with immediately while trust matters are being sorted.

Include specific trust powers in your power of attorney document. Make it crystal clear that your agent can interact with your trust if needed.

Consider a co-trustee arrangement with someone you trust who can manage trust assets immediately in an emergency.

Can a Power of Attorney Amend a Revocable Trust?

Whether your agent can change your trust depends on three key factors:

First, state law matters tremendously. Some states put strict limits on an agent’s ability to modify a trust.

Second, your power of attorney language must specifically grant this power. General authority usually isn’t enough for something this significant.

Third, your trust document provisions might block amendments by anyone but you. Some trusts explicitly say “no agent can change this.”

For your agent to amend your trust, you typically need to specifically grant that authority in your power of attorney. Even then, in some states, your trust must also allow for such amendments. And most importantly, any amendment shouldn’t drastically change who benefits from your trust.

Given the potential for misuse, we typically recommend building in safeguards if you want to allow your agent to make trust changes. For instance, requiring approval from an independent third party or limiting the scope of allowed changes.

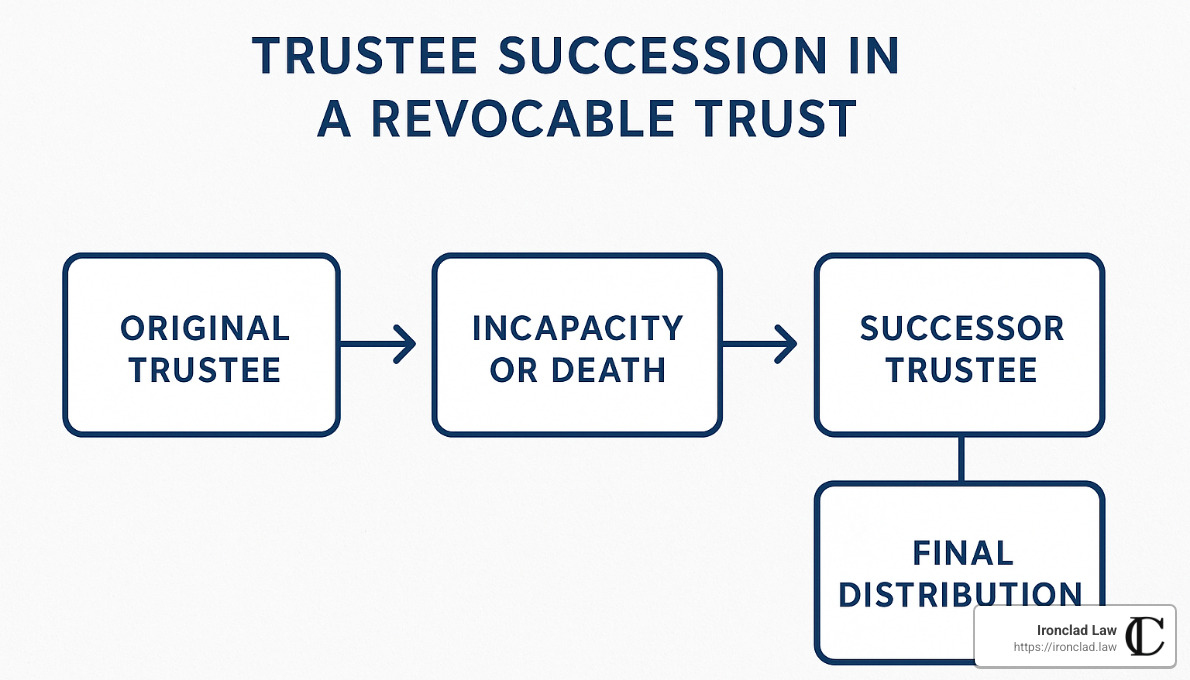

What Happens if the Trustee Becomes Incapacitated?

If you’re serving as your own trustee and become incapacitated, your successor trustee steps in to manage everything – without court involvement. This is one of the biggest advantages of a power of attorney revocable trust strategy.

The transition typically works like this:

Your doctors document your incapacity (usually through formal letters). Your successor trustee then presents this documentation along with the trust document to banks and other institutions. Once they accept their role, they take over management of all trust assets.

This happens privately, without court oversight – unlike the public guardianship process that might be necessary without proper planning. However, there’s an important catch: your successor trustee only controls assets that were properly transferred into the trust before your incapacity.

As one client told me, “When Dad had his stroke, the transition was surprisingly smooth. We had his medical certification, showed the bank his trust documents, and within days I was able to pay his bills and manage his investments. No courts, no lawyers, no delays.”

This seamless transition is why proper incapacity planning requires both documents working in coordination. Your trust handles the assets inside it, while your power of attorney covers everything else – creating a safety net with no holes.

Choosing and Empowering Your Agents and Trustees

Picking the right people to manage your affairs is perhaps the most crucial decision in your estate planning journey. Think of it as casting actors for the most important roles in your life story!

When I sit down with clients to discuss who should serve as their agent under a power of attorney revocable trust arrangement, I always emphasize that character trumps credentials. That trustworthy nephew who always returns borrowed items might be a better choice than your financially-savvy friend with a spotty reliability record.

Integrity should be your north star when making these selections. Someone who will honor your wishes even when no one is looking is invaluable. While financial knowledge is helpful, your agent or trustee can always hire experts for specialized advice – but they can’t hire integrity.

Consider practical matters too. That cousin in California might be your favorite person, but will they be able to handle tasks that require a physical presence if you live in Connecticut? Have honest conversations with potential candidates about what these roles entail. Many people are flattered to be asked but don’t truly understand the time commitment until it’s explained.

Family dynamics also deserve careful consideration. I’ve seen too many families torn apart when one sibling is chosen over another without proper communication. Sometimes naming co-trustees or agents makes sense, but be cautious – this can create deadlocks if they disagree.

Many of my clients choose the same person to serve as both their agent and successor trustee. This approach works beautifully for most families, creating consistency across your plan. However, there are times when splitting these roles makes sense – particularly if the responsibilities would overwhelm one person, or if you want to create a system of checks and balances.

Drafting Language So Your Agent Can Act if Needed

A power of attorney revocable trust strategy is only as effective as the authority you grant. I’ve seen countless cases where families finded too late that a power of attorney lacked critical provisions.

Your power of attorney should specifically authorize your agent to:

Transfer assets to your trust if you haven’t completed the funding process. This “pour-over” authority can be a lifesaver if you become incapacitated with assets still in your individual name.

Make appropriate gifts if that aligns with your wishes. Be specific about whether, to whom, and in what amounts your agent can make gifts. Without this language, your agent’s hands may be tied even when gifting would benefit your overall plan.

Manage your digital life – from social media accounts to cryptocurrency. The digital field is often overlooked in older documents, but these assets can be substantial and complicated to access without proper authorization.

Handle real estate matters with clear authority. In many states, your power of attorney needs specific language for real estate transactions and may need to be recorded with the county land records office.

Steer Medicaid planning if appropriate for your situation. This specialized area often requires explicit authorization for certain types of transactions. Learn more about this on our Medicaid estate planning page.

For personalized guidance on selecting and empowering the right people for these important roles, our lawyers specializing in trusts and wills can help craft documents custom to your unique circumstances.

State-Specific Traps to Avoid in a Power of Attorney Revocable Trust

The legal landscape for power of attorney revocable trust planning varies dramatically depending on where you live. What works perfectly in Florida might be completely ineffective in New York.

Execution requirements are a common stumbling block. Some states require two witnesses for a valid power of attorney, others demand notarization, and some insist on both. Get this wrong, and your document could be worthless when needed most.

Many states have created statutory power of attorney forms that financial institutions in that state are more likely to recognize. While these forms aren’t always required, using them can smooth the path when your agent needs to act on your behalf.

“Hot powers” is a term referring to particularly sensitive authorities that some states require to be explicitly granted. These typically include the power to make gifts, create or modify trusts, or change beneficiary designations. Without specific authorization, your agent may lack critical powers when they’re most needed.

Community property considerations add another layer of complexity in states like California, Arizona, and Texas. Spouses in these states may need special provisions to effectively manage jointly-owned property.

Perhaps the most frustrating issue I encounter in practice is document “staleness.” Although legally a durable power of attorney remains valid until revoked or upon your death, the reality is far different. Banks and financial institutions frequently reject powers of attorney they deem “too old,” even though this practice often contradicts state law.

To avoid this frustration, consider refreshing your power of attorney documents every five years, providing copies to your financial institutions in advance, and creating a revocable trust for your most significant assets to sidestep the power of attorney acceptance problem altogether.

An outdated or inadequate power of attorney revocable trust strategy can leave your loved ones facing expensive court proceedings and delays exactly when they need quick access to help you. Taking the time to get it right now is truly a gift to your family.

Best Practices for Maintaining Your Estate Plan

Once you’ve established your power of attorney revocable trust framework, regular maintenance becomes essential. Think of your estate plan like a garden – it needs ongoing care to flourish and provide the protection you intended.

When to Review Your Estate Plan

Life doesn’t stand still, and neither should your estate plan. I recommend revisiting your documents:

Every 3-5 years at minimum, even if nothing seems to have changed. What feels right at 45 might not make sense at 60.

After significant life events that reshape your family tree – marriages, divorces, births, or deaths. These moments often change not just who matters to you, but how you want to provide for them.

When you move across state lines, your documents need a checkup since estate laws vary dramatically between states. What works perfectly in Florida might create headaches in California.

After meaningful changes in your financial situation – perhaps you’ve inherited assets, started a business, or retired. Each shift might require adjustments to your planning strategy.

For your power of attorney specifically, consider executing a fresh document every 5 years. This isn’t legally required, but practically speaking, financial institutions get nervous about “stale” documents. I’ve seen too many families struggle when a bank rejects a perfectly valid but decade-old power of attorney during a crisis.

For your revocable trust, maintenance means ensuring newly acquired assets actually make it into the trust. The most beautifully drafted trust document accomplishes nothing if your assets aren’t properly titled to it.

Coordinating Trust and Non-Trust Assets

One of the most common estate planning mistakes I see is failing to coordinate what passes through your trust with what passes outside it. This coordination gap can undermine your carefully considered plans.

Start by maintaining a current inventory of everything you own and how it’s titled. This simple step saves your loved ones countless hours of detective work later.

Review beneficiary designations on life insurance, retirement accounts, and payable-on-death accounts to ensure they align with your overall plan. These designations override anything in your will or trust, so consistency matters.

Use a pour-over will as your safety net to catch any assets not properly titled to your trust. Think of it as your backup plan for anything that slips through the cracks.

Consider the tax implications of how assets are titled and who receives them. Sometimes the most tax-efficient approach involves careful coordination between trust and non-trust assets.

Digital assets deserve special attention in your planning. Document your online accounts, cryptocurrencies, and how your fiduciaries can access them when needed.

Certain assets typically bypass both your will and trust:

– Retirement accounts go directly to named beneficiaries

– Life insurance proceeds flow to designated beneficiaries

– Jointly owned property often transfers automatically to the surviving owner

– Payable-on-death accounts move straight to the named recipients

The key is making sure all these designations work in harmony with your bigger estate planning picture. For specialized advice on coordinating these assets, particularly for Medicaid planning, visit our Medicaid estate planning page.

Risks of Relying Solely on a Power of Attorney

While a durable power of attorney provides essential protection, relying on it alone creates several significant vulnerabilities in your plan.

Institutional rejection remains perhaps the biggest practical problem. Despite what the law says, banks and investment companies sometimes refuse to honor powers of attorney, especially older ones. I’ve witnessed heartbreaking situations where families had the right documents but couldn’t use them when needed most.

Limited duration means your power of attorney becomes worthless precisely when many administrative tasks need handling – after your death. This creates a dangerous gap in authority that can leave your family struggling.

Probate exposure continues for assets governed solely by a power of attorney. These documents help during life but don’t change how assets transfer at death.

Potential for abuse exists with any power of attorney. Without proper safeguards and oversight, you’re granting significant authority that could be misused.

Gaps in authority often emerge when certain actions fall outside the specific powers granted in your document. These limitations might only become apparent when your agent tries to help and finds they lack necessary authority.

As one experienced estate planning attorney notes: “Institutional rejection of powers of attorney may contradict the law, but when it happens, families have few practical options. Litigation against major financial institutions costs more time and money than most families can spare during a crisis.”

This reality explains why we typically recommend a combined approach using both a comprehensive durable power of attorney and a properly funded revocable living trust. For more information about comprehensive estate planning, visit our Estate Lawyer services page.

For additional insights on revocable trusts, the Nolo Legal Encyclopedia provides an excellent overview of the basics that can help you understand how these powerful planning tools work.

Frequently Asked Questions about POAs and Trusts

Who controls assets in a funded revocable trust?

When you place assets into a revocable trust, the trustee holds the reins. During your lifetime, that trustee is typically you! This arrangement gives you complete control over your trust assets while you’re able to manage them. You can buy, sell, or use these assets just as you always have—the only difference is they’re now titled in your trust’s name rather than your personal name.

If life throws you a curveball and you become incapacitated, your carefully selected successor trustee steps in to manage everything according to your instructions. They don’t need court permission or oversight—they simply follow the roadmap you’ve already created in your trust document.

After your passing, this same successor trustee continues managing and ultimately distributing your assets to your chosen beneficiaries. This seamless transition is one of the most powerful benefits of a power of attorney revocable trust strategy.

Your power of attorney agent generally can’t manage trust assets because they’re no longer in your personal name—they belong to the trust entity. This distinction might seem technical, but it makes a world of difference when someone needs to help manage your affairs.

Can the same person be both trustee and POA agent?

Absolutely! In fact, naming the same trusted person as both your successor trustee and your power of attorney agent is quite common and often makes perfect sense. This approach creates consistency in who’s handling your affairs and simplifies the process for everyone involved.

Think of it this way: your successor trustee manages assets in your trust, while your POA agent handles assets and matters outside your trust. Having the same person in both roles means they can see the complete picture of your financial life.

That said, sometimes naming different people works better—particularly in complex family situations. You might choose different individuals if:

- You want to create a system of checks and balances

- Different people have skills better suited to each role

- You’re concerned about overwhelming one person with too many responsibilities

- You need to steer delicate family dynamics

If you do name the same person, make sure they understand which hat they’re wearing when signing documents. When acting as trustee, they’ll sign as “Trustee of the [Your Name] Trust,” but when acting as your agent, they’ll sign as “[Your Name], by [Agent Name], Attorney-in-Fact.”

How often should I update my documents?

Life changes, and your estate plan should too. I recommend reviewing your power of attorney revocable trust documents every 3-5 years—or sooner if significant life events occur. Think of it as routine maintenance for your legal protection.

What might trigger an update? Major life changes like marriage, divorce, a new baby or grandchild, or a big move to another state. Financial changes matter too—perhaps you’ve started a business, received an inheritance, or your asset values have changed significantly.

Here’s a practical tip many attorneys won’t tell you: even if nothing in your life has changed, consider refreshing your power of attorney every five years anyway. Why? Banks and financial institutions can be surprisingly stubborn about accepting “older” POA documents, even though legally they remain valid until revoked. A freshly signed POA can help avoid frustrating rejections when your agent needs to use it.

Your revocable trust typically needs updates less frequently, but stay vigilant about funding! Any new assets you acquire should be properly titled in your trust’s name. The most beautiful trust document in the world won’t help avoid probate if your assets aren’t actually in it.

For personalized guidance on maintaining your estate plan, our team at Ironclad Law is always here to help you ensure your documents continue to protect what matters most.

Conclusion

When it comes to protecting your future, having both a power of attorney revocable trust arrangement gives you the most comprehensive coverage. Think of it as wearing both a belt and suspenders – you’re making absolutely sure your pants won’t fall down when you need them most!

At Ironclad Law, we’ve seen how proper planning prevents family stress and financial headaches. Our experience in both courtroom battles and thoughtful estate planning has taught us what works in the real world – not just what looks good on paper.

Here’s what I hope you’ll take away from our discussion:

Your power of attorney is your first line of defense for handling matters outside your trust and managing assets that haven’t been transferred into it. It’s your trusted helper during your lifetime, ready to step in if you can’t make decisions yourself.

Your revocable living trust creates a seamless bridge that carries your wishes from life through incapacity and beyond death. When properly funded, it saves your loved ones from the time, expense, and public exposure of probate.

Both documents need regular check-ups. Life changes, laws evolve, and what worked perfectly five years ago might need adjustments today. Think of it like servicing your car – preventative maintenance prevents breakdowns when you least expect them.

Don’t forget about coordinating everything. Your beautiful trust won’t help with assets that aren’t properly titled in its name. Your retirement accounts, life insurance, and jointly-owned property all need to work in harmony with your main estate plan.

Perhaps most importantly, choose your helpers wisely. The best legal documents in the world can’t make up for selecting the wrong people to carry out your wishes. Integrity matters more than financial expertise – you want someone who’ll do what’s right, not what’s easiest.

Estate planning isn’t just about distributing property or avoiding taxes. It’s about creating peace of mind – knowing you’ve done everything possible to make things easier for the people you love. It’s about maintaining your dignity and independence even if illness or injury strikes. It’s about leaving a thoughtful legacy rather than a mess to clean up.

With proper planning through a power of attorney revocable trust approach, you can face the future with confidence, knowing you’ve put protections in place for whatever life brings.

For personalized guidance on creating or updating your estate plan, our estate lawyer team is ready to help you steer these waters with clarity and confidence. We believe estate planning should be accessible, understandable, and actually work when your family needs it most.